Senior leadership at the Securities and Exchange Commission (SEC) has vowed to use section 20(b), an obscure section of the Securities Exchange Act of 1934, to charge individuals who may have had some role in a corporate disclosure but were not the requisite “makers” of the statement.

Senior leadership at the Securities and Exchange Commission (SEC) has vowed to use section 20(b), an obscure section of the Securities Exchange Act of 1934, to charge individuals who may have had some role in a corporate disclosure but were not the requisite “makers” of the statement.

The ramifications are significant for directors, including members of the audit committee, and officers who may have reviewed or assisted in the preparation of corporate disclosures. SEC Chair White and Enforcement Director Ceresney both indicated that the SEC will pursue gatekeepers, including directors, and the SEC recently charged the chair of an audit committee for allegedly failing to act promptly enough to investigate red flags.

For decades, the SEC has used section 20(a) to pursue individuals for secondary liability, but section 20(a) requires the SEC to establish that someone else committed an underlying violation and that the individuals controlled the primary actor — both of which are high hurdles. In 2011, the Supreme Court in Janus Capital Group, Inc. v. First Derivative Traders held that only the “maker” of a statement may be liable for securities fraud and that the maker is the person or entity with “ultimate authority” over that statement.

The Court explained that other persons who contributed to the creation of a statement (or corporate disclosure) may avoid liability if they lacked the requisite “ultimate authority.” The Court did hint, however, that section 20(b) of the Exchange Act may address individuals who assisted in creating the statement but lacked “ultimate authority.”

Joseph Brenner, the Chief Counsel in the SEC’s Division of Enforcement, has stated that he is “fairly confident and hopeful” that the SEC soon would use section 20(b) to pursue primary liability against an individual, such as a director, because that individual had some role in the false or misleading statement, including merely reviewing the statement in the context of an audit committee meeting or similar meeting of the board of directors.

Our View

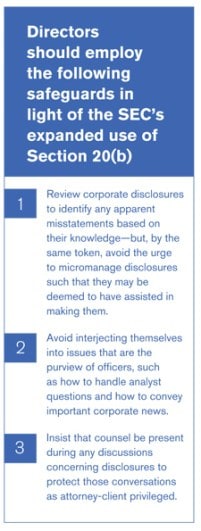

The SEC’s position is unsettled. However, we believe existing case law suggests that the SEC will have difficulty in court if it decides to use section 20(b) in such an aggressive manner. In light of the significance to directors of the aggressive SEC stance, we think it would be prudent for boards to employ safeguards (see sidebar).

Bradley J. Bondi leads the Securities Enforcement and Investigations Group at Cadwalader, Wickersham & Taft and is a partner in the White Collar Defense and Investigations and Securities Litigation practices. He focuses on a wide range of complex civil and criminal matters involving securities and financial laws, corporate governance, and business laws. Bondi represents boards, companies, financial institutions, and individuals in internal investigations, domestic and foreign government inquiries, and adversarial proceedings, including enforcement actions involving the Securities and Exchange Commission (SEC) and the Department of Justice (DOJ), and complex private litigation from trial to appeal. In a counseling role, he advises boards of directors, audit committees, special committees, and senior management of public companies and financial institutions on matters of corporate governance, securities and financial regulation, fiduciary duties, compliance with the Sarbanes-Oxley and Dodd-Frank Acts, and crisis management. Email Bondi at [email protected]